Week in Energy

Monday 31/07 – The European Commission announces it will take action to tackle pollution from Large Combustion Plants, such as power stations and district heating plants. The Business Energy Efficiency programme in Cambridgeshire announces it has already supported 36 SMEs to help cut their carbon and identified over £200,000 in savings. Ofgem commits to continued engagement on European issues whilst the UK remains in the European Union in its annual National Report to the European Commission.

Tuesday 01/08 – New government statistics find the number of Energy Performance Certificates lodged for non-domestic properties rose 7% in the second quarter of 2017, when compared to the same period a year earlier. The Grantham Research Institute argues that the best long-term strategy for managing energy costs is to reduce energy waste.

Wednesday 02/08 – Scottish Business, Innovation and Energy Minister Paul Wheelhouse announces a £1.5mn investment into the Offshore Wind Accelerator. The Competition and Markets Authority raises competition concerns over the Wood Group’s planned purchase of Amec Foster Wheeler.

Thursday 03/08 – A group of industry experts warn the UK energy system is in flux and that large utility companies must be flexible if they are to “survive and thrive”. Ofgem confirms that National Grid Electricity Transmission should form a legally separate electricity system operator by 1 April 2019. The latest wave of the BEIS Public Attitudes Tracker reveals a significant decrease in public concern over energy security.

Friday 04/08 – Ofgem officially launches its Significant Code Review for the planned Targeted Charging Review, aiming to consider reform of residual charging for transmission and distribution, for both generation and demand, to ensure it meets the interests of consumers, now and in future. Transport for London announces £4.48mn will be allocated to London boroughs to install electric vehicle charging infrastructure on London streets.

Back to top

Policy 1 | Coal generation continues to fall

BEIS released its Digest of UK Energy Statistics (DUKES) figures on Thursday, 27 July, revealing a steep fall in coal generation in 2016.

The DUKES document provides a comprehensive overview of all energy statistics in 2016. One of the major trends was that coal output decreased to “record low levels”, more than halving from 76TWh to 31TWh. The fall was compensated for by a boost in gas generation, which rose from a generation share of 29% in 2015 to 42% in 2016, totalling 143TWh. While fossil fuels remain the dominant source of energy supply, they now account for a record low level (81.5%).

Renewables essentially matched their 2015 share. This meant renewables proportion of generation was stable at 24.5% for 2016, 0.1% lower than in 2015. Less favourable weather conditions for wind and solar counteracted increased renewable capacity.

Meanwhile, low carbon electricity’s share of generation grew slightly, reaching a landmark figure. From 46.2% in 2015, it hit a record 46.5% in 2016. Nuclear generation was found to be up 2.7% compared to 2015. The report said this was because of improved availability along with fewer outages.

Final electricity consumption remained at broadly the same level as since 2014. In 2016, it stood at 304TWh – the lowest since 1995. Industrial consumption fell 1.2% compared to 2015, marking a 20% fall since 2000, while transport consumption rose by 3.4%. The number of electric vehicles increasing from 29,000 to 39,000 was given as a reason for this.

The UK has now exceeded its third interim target against the EU Renewable Energy Directive, with DUKES confirming 8.9% of total energy consumption came from renewable sources in 2016. This was up from 8.2% in 2015. Over 2015 and 2016, renewables averaged 8.5% against the 7.5% target.

The figures also revealed that the UK remains a net importer of electricity. In 2016, net imports contributed 4.9% of electricity supply. While remaining a net importer, net imports did fall 16% for the year compared to a record 21TWh in 2015.

The document also noted that nuclear outages in France saw exports increase 21%. The interconnector between France and UK was damaged in November 2016, halving its capacity for the rest of the year.

The UK’s total electricity supply was slightly lower in 2016 (357TWh) than 2015 (360TWh). BEIS explained that supply is driven totally by demand, with the impacts of improving energy efficiency and warmer overall temperatures seeing demand fall since 2005.

Furthermore, provisional estimates from the department found overall emissions fell by nearly 30mn tonnes of carbon dioxide (MtCO2) to 374.1MtCO2 between 2015 and 2016. This is a fall of 7.4% and attributed mainly to changes in electricity generation.

Back to top

Policy 2 | Non-domestic RHI installations see drop

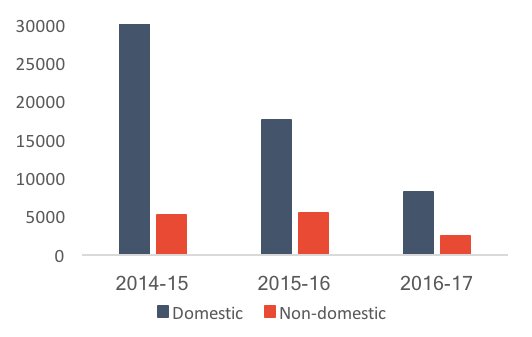

Figures released by energy regulator Ofgem have shown that the number of installations accredited under the Non-Domestic Renewable Heat Incentive (RHI) scheme fell sharply during 2016-17.

In its Non-Domestic Renewable Heat Incentive (RHI) Annual Report, published on Wednesday, 26 July, Ofgem revealed that the number of installations accredited in the 2016-17 financial year fell to 2,407. This is down by over half on the two previous years, (5,394 in 2015-16 and 5,184 in 2014-15) and puts the number of accreditations at a similar level as those seen in 2013-14 (2,561). To date the scheme has accredited 16,662 installations, with a total installed capacity of 3,207MW.

The Non-Domestic RHI is a government led environmental programme designed to increase the uptake of renewable heat by businesses, the public sector and non-profit organisations. The scheme was set up in 2011 and contributes to the UK’s target of meeting 15% of energy demand with renewable sources by 2020.

The majority of the installations (89.6%) were solid biomass boilers, with the second largest ground source heat pumps at 4.2%. The remaining installations were made up of biogas (2.1%), air source heat pumps (1.7%), solar thermal (1.6%), water source heat pumps (0.4%), biomethane (0.4%) and solid biomass combined heat and power (0.1%).

Figure 1: Number of RHI installations accredited since 2014-15

Ofgem also noted some changes that have been made over the past year to the Non-Domestic RHI Regulations. In August 2016 BEIS introduced an amendment to the scheme affecting how payments are calculated for solid biomass CHP installations with a tariff start date on or after 1 August 2016 and a power efficiency less than 20%. For installations with a tariff start date on or after 1 January this power efficiency requirement was changed to 10%.

In December 2016 BEIS announced reforms to the RHI scheme regulations. These reforms were expected to come into force in Spring 2017, however the parliamentary process was delayed due to the General Election. BEIS will be providing an update on the progress of these reforms in due course.

The report also set out some wider industry changes that may impact some participants of the scheme. These included that the Sustainable Fuel Register (SFR), a new fuel list for non-woody biomass fuels was approved by the government and fees for applicants registering on the Biomass Suppliers List were introduced from 1 January.

Back to top

Policy 3 | Government and energy industry face big decisions after proposed 2040 ban on diesel and petrol car sales

On Wednesday, 26 July, the government announced plans to ban the sale of new diesel and petrol cars by 2040.

The proposals have been welcomed by a wide range of organisations including National Grid, but concerns have been raised with regards to the impacts on electricity demand. In its Future Energy Scenarios, released in July, National Grid said electric cars could create the need for 3.5-8GW of additional capacity by 2030. This is more than what the Hinkley Point C nuclear project will add to the system and on top of the current peak demand of 60GW.

National Grid said government and industry face “big decisions” as to how this extra power is provided, alongside how demand is managed. Potential options include smart meters and time-of-day tariffs which could incentives owners to charge when substantial wind and solar power is being produced and electricity is cheaper.

Another solution is energy networks managing demand through automatic time-shift changing. This involves a car plugged in at home around 6pm not actually being charged until the early hours of the morning, when demand is low.

James Court, Head of Policy at the Renewable Energy Association, said: “We need smart vehicle charging and price-reflective tariffs if the future electric fleet is to be a huge benefit and not a hindrance to our grid.”

Back to top

Policy 4 | Non-domestic Energy Performance Certificates increase

Published on Tuesday, 1 August, new government statistics have shown the number of Energy Performance Certificates (EPCs) lodged for non-domestic properties increased in the second quarter of 2017 compared to the same period a year earlier.

EPCs use a rating scale to indicate the energy efficiency of a building. The scale goes from A+ to G, with an A grade being “highly efficient” and G being “low efficiency”. The majority of non-domestic properties were placed in Band D (35%). Band D is regarded as average, as well as being the required level to have solar panels installed and receive the standard rate from the Feed-in Tariff.

Around 18,000 EPCs were lodged in the quarter. The document also found that for the 12-month period ending in June 2017, 70,000 EPCs for non-domestic properties had been lodged. This marked an increase based on the same period for 2016.

Only 3% of properties were given an A+/A grade. The fewest properties were placed in Band B and above (11%), though the majority attained at least the average with 28% handed a certificate placed below D.

Industry 1 | Onshore wind could thrive with “market stabilisation” CfD

Onshore windfarms could be delivered for an administrative strike price of between £50-55/MWh, using a “market stabilisation” Contract for Difference (CfD), according to a recent research by consultancy firm Arup.

The report – Enabling Investment in Established Low Carbon Electricity Generation – found that onshore wind has the potential to become the lowest-cost form of energy generation in the UK if it is included in a CfD mechanism, providing revenue stabilisation and mitigation of the financial risks for investors.

The current framework of the CfD mechanism provides a steady revenue stream to generators, with contracts auctioned through a competitive process and only the most cost-effective projects winning contracts. The creation of a subsidy-free, “market stabilisation” CfD is thought possible for onshore wind, with stakeholders suggesting that it could be the first renewable generation technology to “stand on its own two feet,” as it currently has the lowest levelized cost of electricity of all renewable generation. Current government policy is that no new support will be provided for onshore wind.

An administrative strike price (ASP) represents the maximum support, presented on a price per MWh basis, that the government is willing to offer developers for each technology in a given delivery year. To calculate the appropriate ASP for onshore wind under a market stabilisation CfD, Arup explored two methodologies. Under the first methodology, it used government estimates on how wholesale prices will change over time and calculated an indicative administrative strike price of £47/MWh for onshore wind. When stress testing variables against different forecasting scenarios, ASPs ranged from £38/MWh to £54.4/MWh.

The second method compared onshore wind against the costs of constructing a new combined-cycle gas turbine (CCGT), on the assumption that it costs £476/kW for new CCGT plant in 2020. Testing of this method showed that the ASP varies considerably based on wholesale gas costs and the prevailing carbon price; ranging between £41.4/MWh and £60.2/MWh. Overall, the methodology gave an indicative ASP of £52.5/MWh.

By comparing the results of the two different methodologies, Arup recommended an ASP of between £50-55/MWh (at 2012 prices), assuming that the variables included follow a central case scenario. This is already substantially below the lowest strike price for onshore wind seen in the February 2015 CfD auction, of £79.23/MWh. Arup also found that there are some highly efficient onshore windfarms already achieving a levelized cost of electricity of £50/MWh which would merit an ASP in the region of the proposed £50-55/MWh.

Beyond wholesale costs, the report identified the pivotal role that flexibility in the National Grid will play. It cited a study undertaken by Imperial College London which found that the system integration costs of onshore wind fall from £10.2/MWh to £7.6/MWh if action is taken to modernise the grid and make it more flexible. Commenting on the report, Filippo Gaddo, Associate Director at Arup, said that, “Access to a Market Stabilisation CfD mechanism [for onshore wind] would make a significant difference to driving efficiency – ensuring that the UK’s transition to low-carbon generation progresses in the most cost-effective manner.”

Industry 2 | National Grid sets final gas transmission charges from 1 October

National Grid has issued confirmation on the changes to gas transmission charges that will come into force on 1 October.

Britain’s gas transmission network, the National Transmission System (NTS), is the high pressure gas network which transports gas from the entry terminals to gas distribution networks, or directly to power stations and other large industrial users. Increases in costs are ultimately passed to end users.

The notice of revised charges, issued 31 July, made amendments from the previous period following updated demand forecasts. This included greater demand for gas for use in power generation, as well as reductions in capacity bookings in the July 2017 application window. Allowed transportation owner (TO) revenue has decreased by £1mn since last year to £848mn. The national transmission system (NTS) TO entry commodity charge levied on entry flows will be reduced to 0.0509p/kWh, a decrease of 4%. This will effectively reduce revenue collected from entry commodity charges by £17.4mn. The NTS TO exit commodity charge will increase slightly from 0.0234p/kWh to 0.0235p/kWh due to reductions in capacity bookings in the July 2017 exit capacity application window.

The system operator (SO) allowed revenue is forecast to decrease by £5mn to £210mn. The NTS SO commodity charge, as applied to both entry and exit flows, is set at 0.0106p/kWh, an increase of 1% from the previous rate. This will mean a £2.4mn reduction in revenue from this source. The St. Fergus compression charge, which recoups costs from gas shippers for the different pressure tier arrangements at the terminal, will increase by 1% to 0.0104p/kWh.

Industry 3 | WindEurope praises wind growth but warns of market concentration

WindEurope, which works to promote wind power, published an update on the installation of wind-powered generation assets across the EU in the first half of 2017.

It found that a total of 6.1GW of additional wind energy capacity was installed, with 4.8GW based onshore and the remaining 1.3GW coming from offshore projects. However, WindEurope Chief Policy Officer, Pierre Tardieu cautioned against the geographic concentration taking place. He said: “We are on track for a good year in wind capacity installations but growth is driven by a handful of markets. At least 10 EU countries have yet to install a single MW so far this year.”

The figures show that, for onshore installations, 3.9GW of the 4.8GW installed are sited in Germany, the UK and France, with these first two countries installing around 71% of all EU onshore wind projects in the first half of this year. Equally, all of the 18 offshore projects installed were based in just four countries; Germany, the UK, Belgium and Finland. Over 86% of the offshore projects were based in Germany and the UK.

Looking ahead to future investments, asset financing across the EU was down on 2016, and was also showing signs of concentration, with 53% focusing on the German market. WindEurope highlighted that this trend could be further heightened as the full impacts from the end of the renewable obligation scheme in the UK begin to be felt.